A falling inflation rate, an abundance of job opportunities, and a pessimistic outlook might fuel future rises.

Are the bears finished eating? As a result of the 2% gain on Wednesday, the Dow Jones Industrial Average is now 20% higher than its lows in October, which satisfies the standard definition of a bull market.

The fact that all of the major stock averages and bonds are still showing big losses year-to-date, that cryptocurrencies are collapsing, and that people are feeling the effects of high inflation despite worries about a recession keeps many investors from being in the mood to celebrate. Thursday's market action mirrored that level of mistrust. The major market indices finished the day with only minor shifts as investors awaited a signal from tomorrow's employment report.

According to the results of a recent study conducted by the American Association of Individual Investors (AAII), individual investor sentiment continues to be distinctly gloomy. At the end of November, market bears made up more than 40% of respondents, while bulls made up less than 25%.

This is a bearish indicator that suggests more people may become bullish on equities, which would provide extra gasoline for the surge. Here are some further arguments in favor of the possibility that stocks may finish a difficult year on a positive note.

KEY TAKEAWAYS

- Since the middle of October, stock markets in the United States and around the world have staged spectacular comebacks.

At the end of November, the Dow Jones Industrial Average had gained 20% from its low point.

- Despite the fact that confidence among investors has improved over the course of the past month, pessimistic sentiment persists.

- The United States had lower inflation in October, raising hopes that rate hikes may be coming to an end soon.

- Both the labor market and the earnings of businesses have maintained their historically high levels.

- While Europe is working to address its energy issue, China has relaxed some of its COVID rules.

The rate of inflation is decreasing.

- Inflation is still high, according to Federal Reserve Chair Jerome Powell, who emphasized this point in a speech he gave on Wednesday. The Fed's preferred inflation gauge, the personal consumption expenditures (PCE) price index, has increased by 6% over the course of the previous year.

- Despite this, the statistics that was made public on Thursday revealed that the index and the consumer price index (CPI), another measure of inflation, both climbed by a less amount than was anticipated in the month of October.

The core PCE inflation rate, which strips out the effects of food and energy prices, increased by only 0.2% from the previous month in October, marking a significant drop from September's gain of 0.5% on the same basis.

As Powell pointed out, this is only one month, but if you add 11 more months like this one, you will end up with annual inflation of 2.4%, which is not much more than the Fed's long-term target of 2%.

Stocks rallying could last 1-2 months, maybe even into Dec. No guarantees of that - but that would be very typical end of year.

— Alpha SkyFi 🌐 (@BlokTech_io) October 26, 2022

However, after this Stock Market rally, I'm pretty sure we're headed into a deeper, extended Bear Market.🐻$SPY $SPX #SP500 S&P500 $QQQ Nasdaq Nas100 pic.twitter.com/SepxUxiRxC

Additionally, supply-side tensions are beginning to ease. The inflation that occurred over the previous year corresponded with widespread supply interruptions that have largely subsided, and the jump in the price of gasoline in the United States that followed Russia's invasion of Ukraine has also been reversed.

The inflation that occurred over the past year took place during a time when interest rates were much lower. This occurred despite the fact that the Federal Reserve raised its benchmark fed funds rate from almost zero in March to over 4% presently.

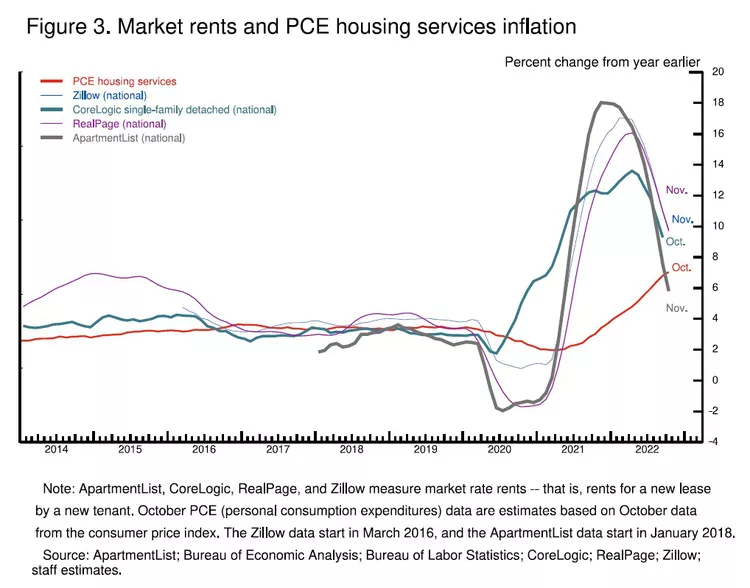

As a direct consequence of this, some leading indications of future inflation, such as apartment rents and port unloading waits, have recently experienced a dramatic deceleration.

The question that needs to be answered is whether or not there will be a decline in prices for services notwithstanding the historically robust labor market.

The State of the Economy Remains Stable

In the first three quarters of this year, the Federal Reserve raised interest rates, which had the effect of slowing down the rate of economic expansion in the United States. It is anticipated that the fourth quarter would only show a slight improvement.

And as Powell reaffirmed on Wednesday, the full consequences of previous rate hikes haven't propagated through the economy quite yet, which provides a prolonged short-term headwind. This is a headwind that will continue in the near future.

https://www.investopedia.com/the-express-podcast-episode-99-6455994

However, recent activity in the stock market suggests a degree of comfort regarding the impact that the rate hikes have had to this point. The labor market is still historically tight, and the initial unemployment claims data that was released on Thursday confirmed that employers are still reluctant to fire workers since there are still so many open positions that have not been filled.

It is quite improbable that consumer spending, which accounts for two-thirds of U.S. GDP, would decrease significantly so long as unemployment remains at historically low levels and wage growth continues to outpace the trend.

The decline in spending seen in October was mostly brought on by consumers with lower incomes, who were the hardest hurt by the growing cost of basics. Recent drops in the price of gasoline should be of assistance on this front, as would a reduction in the pace of inflation in the following year.

The spending habits of businesses have likewise remained stable. As a result of the increases in the prices of their goods, large corporations that are publicly traded are continuing to enjoy historically robust profit margins.

Earnings for the S&P 500 were up 9.2% year-over-year in the third quarter, and although the current estimate for the fourth quarter is that it will be down slightly year-over-year, there is a good chance that it will end up showing a gain, as 70% of S&P 500 companies beat estimates in the third quarter.

In the previous year, a broader measure of corporate profits claimed its greatest percentage of domestic income since 1929. This trend continued in the previous year as well.

There have already been layoffs made by companies of all sizes, including those in the technology industry, and there may be more to come. There is a possibility that the current slight decline in expenditure on technology will become more severe. However, since Powell has indicated that the federal funds rate likely top out near 5%, this may potentially leave the Fed with only 50 basis points of additional increases beyond December. The longer a prolonged recession is avoided by the economy, the higher the hopes are that the Federal Reserve will be able to successfully construct a historically elusive "soft landing."

The Risks of Memo, FOMO, and Your Career

The market's recovery from the lows it reached in the middle of October gives stocks a great deal of short-term momentum. The Dow Jones Industrial Average has been the leader of the pack, but the Standard & Poor's 500 Index has recaptured its 200-day moving average. This is a highly monitored trend indicator that limited the index's recovery in August. If the S&P can maintain and extend its breakthrough from this week into late December, it may be able to persuade additional market players that the bear market of 2022 has come to an end.

The recent surge in short-term momentum presents a conundrum for fund managers, a significant number of whom have had a challenging year. Everyone stands an equal chance of experiencing financial hardship in the event of a bear market. It is both a more potent bonus and a greater danger for one's career to underperform one's competition since one did not ride the year-end rally with sufficient intensity. In the event that market gains persist, retail investors can potentially acquire the "fear of losing out" fever.

Clearing of the Global Storm Clouds

The severe deceleration in economic development that has been observed in Europe and China this year is one of the primary factors that have contributed to the importance of equity market concerns. Because of Russia's invasion of Ukraine, energy and electricity prices across the continent have skyrocketed, which has wreaked havoc on the finances of European countries. This year, China's development rate has slowed drastically, largely due to the fact that the government in Beijing has ordered prolonged and broad lockdowns in an effort to prevent the spread of COVID-19.

On each side, there is now reason to have renewed optimism. Europe has ended its long-standing reliance on natural gas imported from Russia and has made efforts to mitigate interruptions in the region's electrical grid. Recent growth indicators imply that the recession may not be as severe as was previously feared, despite the fact that it is still anticipated that the continent would have a recession the following year.

Even before the severe quarantines became the focus of significant popular demonstrations in China a week ago, the Chinese government had already begun looking into potential departure strategies from its Zero-COVID policy. It would appear that those activities have gained momentum as a direct result of the demonstrations.

Even though the resiliency of Europe and China's about-face do not eliminate the chances of additional rate hikes, recession, and ongoing Russian aggressiveness, they do limit the downside. They have also caused a historically strong dollar to lose some of its lustre during the previous month, easing inflationary pressures abroad.

During the month of November, developed overseas markets had a better performance than the S&P 500 index. The most recent increases on the market have been led by companies in the industrial, materials, and financial sectors in the United States.

One does not make purchases in these markets in the run-up to a recession.

Sentiment Remains Subdued

In spite of users' high risk aversion, the results of the latest monthly edition of the Investopedia investor poll reveal that readers are gradually becoming more bullish on equities. The same pattern can be seen with professional investors as well.

There have been a number of surveys recently that have shown the majority of market participants are still doubtful that recent market advances will continue. This leaves a lot of leeway for equities to soar even more if the mindset turns in the opposite direction.

The Crux of the Matter

None of the aforementioned can absolutely guarantee that the bear market is over. The most significant danger to ongoing expansion is still posed by the lingering consequences of earlier interest rate increases. However, the fundamentals that support consumer and business spending have not changed for the time being, and many investors continue to underestimate the current rebound despite the fact that it has occurred. That sounds like a good recipe for additional increases in the stock market over the next few months.

A Digital Wallet for All of Your Web3 Needs is Provided by Our Sponsor

Accessing a wide variety of DeFi platforms, ranging from cryptocurrencies to NFTs and beyond, is much easier than you might imagine. When you trade assets and store them with OKX, a renowned provider of digital asset finance services, you have access to the highest possible level of protection. You can also link existing wallets and be entered into a drawing for a chance to win up to $10,000 if you make a deposit of more than $50 through the purchase of cryptocurrency or a top-up within the first 30 days after registering an account. Find out more, and sign up right away.